Planopedia

Clear, accessible definitions for common urban planning terms.

What Is Redlining?

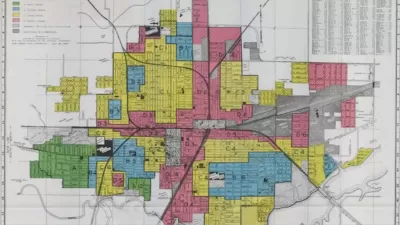

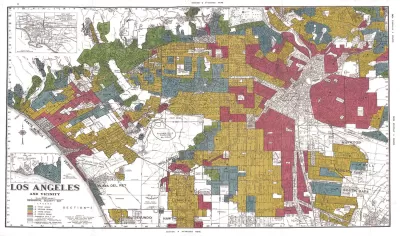

Redlining is the practice of restricting investment in areas deemed high-risk by banks. The term refers to the red color used to denote undesirable areas on maps used by lending institutions to determine loan eligibility.

Redlining, which perpetuated housing segregation by encouraging banks to deny mortgages in "hazardous" areas occupied by "undesirable populations," came about as a result of the passage of the 1934 National Housing Act and the creation of a federal mortgage agency. Initially developed as guidelines for the federal Home Owners' Loan Corporation (HOLC) for managing their limited budget and assessing credit worthiness, color-coded "residential security maps" rated neighborhoods using categories like age and condition of housing, proximity to amenities and transportation, nearby land uses, income level of current residents, and, most controversially, ethnic composition. The Federal Housing Administration (FHA) explicitly cited the presence of "incompatible racial and social groups" as a factor in downgrading areas.

The maps defined credit risk by neighborhood rather than based on an individual's ability to repay their loan, entrenching discrimination in the poorest areas. These maps reflected a broader pattern of discrimination, with private lenders engaging in similar practices, which resulted in segregated housing markets and reduced opportunities for minority families to own homes and build wealth and equity.

Although it was prohibited by the Fair Housing Act of 1968, redlining has had long-lasting impacts that continue to reverberate throughout American neighborhoods. Today, three-fourths of neighborhoods designated as "hazardous" on HOLC's maps remain poorer than others. In Macon, Georgia, the city with the highest rate of redlined neighborhoods in the 1930s (65%), the poverty rate today is close to 25% overall and 33% for the Black population. Neighborhoods rated "Grade A" in the 1930s, on the other hand, are now 91% upper income and almost entirely white.

Owning a home in a redlined area could also make it harder to sell, leading to a loss of potential income and equity. A study by real estate app Redfin found that "Black families have lost out on at least $212,000 in personal wealth over the last 40 years because their home was redlined." Today, the median white family holds roughly 10 times the wealth of the median Black family. Housing discrimination has also led to predatory practices such as "reverse redlining," engaging in predatory lending in previously redlined areas by aggressively targeting Black and Latino borrowers. While borrowers can now purchase homes in areas deemed off-limits in the past, they pay excessively high rates and risk foreclosure.

Meanwhile, researchers have come to the conclusion that place matters greatly in almost all aspects of life and well-being, including health, job opportunities, earning potential, and life expectancy. During the COVID-19 pandemic, low-income zip codes have suffered disproportionately high rates of infection and death. Therefore, the effects of redlining and continued discrimination in housing policies continue to harm communities of color and low-income Americans, keeping many households trapped in a cycle of poverty and poor health.